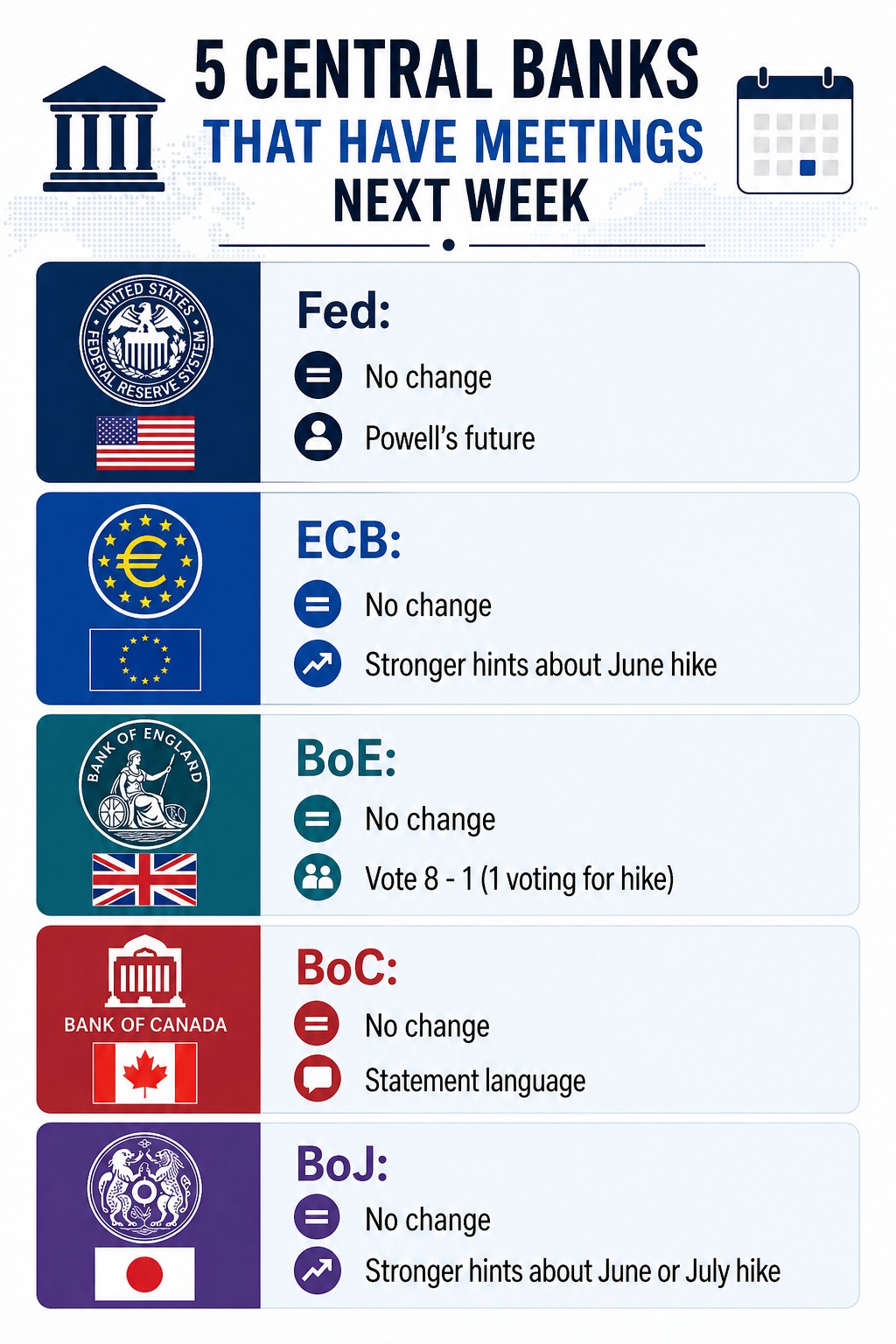

Fed, ECB, BoE BoC and BoJ meetings coupled with preliminary Q1 GDP prints from the US and Eurozone as well as inflation data from the Eurozone and Australia will highlight this very important week. Additionally, we will get earnings from Big Tech, Amazon, Google, Meta and Microsoft report on Wednesday after the close. On top of that, there will be news regarding US – Iran war which will add to the volatility.

USD

Iran refused to participate in negotiations until the US blockade of Straight of Hormuz is lifted. President Trump extended ceasefire indefinitely stating that Iran’s leadership is fragmented and that US military managed to destroy Iranian military and navy. Later on Iran has received some signs that US might be ready to break the blockade. Trump stated that he is in no rush to make a deal and that deal will be made only when it is “appropriate and good for the United States of America, our Allies and, in fact, the rest of the World.” Iran retorted by deploying fresh mines into the Straight.

Fed Chairman nominee Kevin Warsh testified in front of the Senate where he stated that US needs fundamental policy reforms to fix inflation adding that he wants new inflation framework. He did not comment on rate cuts but he stated that Fed will need to find a way to lower its balance sheet. Apple CEO Tim Cook announced that he will be stepping down and will assume a role of Executive Chairman. He will be replaced on September 1 by John Ternus former VP of hardware engineering. This is the first change in Apple’s leadership since 2011 when Cook replaced Steve Jobs as the new CEO.

Retail sales report for the month of March echoed a truism “never underestimate the spending power of US consumer.” Headline number showed 1.7% m/m increase, higher than 1.4% m/m as expected and jump from 0.6% m/m in February. Ex autos category fared even better rising 1.9% m/m vs 1.4% m/m as expected. Control group, excluding volatile components and used for GDP calculation, rose 0.7% m/m vs 0.2% m/m as expected for the strongest increase since June of 2025. Digging into the details we can see that spending at gasoline stations surged 15.5% m/m due to rising gasoline prices and it was followed by gains in department stores, furniture stores and retail and food services. Miscellaneous store retailers were the only category that was down compared to the previous month while food services & drinking places, a good proxy for discretionary spending, ticked up 0.1% m/m.

The yield on a 10y Treasury started the week at 4.25%, rose to 4.34% and finished the week at around 4.31%. The yield on 2y Treasury started the week at 3.71%, rose to 3.85% and finished the week at around 3.78%. Spread between 2y and 10y Treasuries started the week at 54bp and finished the week at 53bp. FedWatchTool sees the probability of a 25bp rate hike at May meeting at around 1% while probability of no change is at around 99%. WTI had another volatile week dropping as low as $85 on the market open and then surging to over $100 only to finish the week at around $97. S&P and NASDAQ reached new all-time-highs.

This week we will have FOMC meeting, advanced Q1 GDP print as well as ISM manufacturing PMI. There will be no change to rate so the focus will be on Powell’s press conference and whether this will be his last as Fed Chairman and will he remain on as a Governor.

Important news for USD:

Wednesday:

Fed Interest Rate Decision

Thursday:

GDP

Friday:

ISM Manufacturing PMI

EUR

Preliminary PMI data for the month of April saw manufacturing rose to 52.2 from 51.6 in March while markets were bracing for a decline to 50.9. New orders index surged but it seems to be due to frontloading in order to avoid any further supply chain disruptions coming in the future. Services sector plunged into contraction with a 47.4 print after 50.2 the previous month. The sector is hit hard by the ongoing US – Iran war as evidenced by a plunge in business activity not seen since COVID started in early 2021. The report notes that input costs and selling prices have surged to levels, if we exclude COVID, not seen since 2000. Eurozone started Q2 on a week note and if this data point gets extrapolated it will mean a 0.1% decline of second quarter GDP. Composite was dragged down as well into contraction with a 48.6 print for the lowest print in past sixteen months. German Ifo business climate index slumped in April to the lowest level since October of 2022 due to the growing uncertainties caused by Middle East war.

This week we will have ECB meeting as well as preliminary Q1 GDP and April inflation data. Markets expect ECB to stay on hold next week and hike in June so the communication will be closely monitored.

Important news for EUR:

Thursday:

ECB Interest Rate Decision

GDP

CPI

GBP

March employment report saw economy lose another 11k jobs with February reading being revised down to show 6k job loses. ILO unemployment rate for the period of three months to February showed a big drop to 4.9% from 5.2%. However, the details of report show that the drop was due to a rise in “economic inactivity”, which means increase in people neither in work nor seeking work. Wages continued to decline but at a slower pace with regular weekly wages coming in at 3.8% 3m/y and ex bonus at 3.6% 3m/y. Wage growth in the public sector rose 5.2% 3m/y while it rose 3.2% 3m/y for the private sector. When inflation is taken into the picture real wage growth is barely positive. ONS has once again added a caveat to this reading stating that there are data quality issues and that this report should be interpreted with caution.

Headline CPI in March rose to 3.3% y/y as expected from 3% y/y seen in both January and February on the back of rising energy costs. So far inflation is contained in energy prices as core print ticked down to 3.1% y/y from 3.2% y/y the previous month. However, services inflation rose to 4.5% from 4.3%, although due to higher air fares which were affected by the higher fuel prices.

April preliminary PMI numbers showed encouraging signs. Manufacturing jumped to 53.6 from 51 in March beating expectations of a drop to 50.3. Services rose to 52 from 50.5 the previous month also beating expectations of a 50 print and combined they keep composite rising and settling at a healthy 52. Input prices surged and report clarifies that energy prices were not the only reason for rising prices as there were also visible increases in prices of “wide variety of goods and services.”

This week we will have BoE meeting. There will be no change to rate but the vote will be scrutinized, most likely 8-1 in favour of no change with one member voting for a rate hike, as well as further hints about potential rate hikes later in the year to fight off inflationary pressures.

Important news for GBP:

Thursday:

BoE Interest Rate Decision

AUD

Aussie has enjoyed moments of risk on in the markets and has suffered through the moments of risk off. Volatility caused by US – Iran war is swinging AUD from one extreme over to the other. We will get much more clarify on currency’s direction next week once we get inflation data as RBA is focusing primarily on inflation.

This week we will have quarterly inflation data which is of paramount importance for future RBA moves.

Important news for AUD:

Wednesday:

CPI

NZD

Q1 inflation report saw prices increase 0.9% q/q and 3.1% y/y, higher than 0.8% q/q and 2.9% y/y as expected. The report flags electricity (12.5%) and petrol prices as main drivers of rising prices. Inflation was seen in so-called non-tradables, which refer to “goods and services that are primarily produced and consumed domestically, with prices driven by local economic conditions rather than global markets.” This makes it two quarters in a row of inflation sitting slightly above bank’s target of 1-3% which increases chances of RBNZ hike. The economy posted first trade surplus since May of 2025 as surge in exports overshadowed jump in imports.

CAD

March inflation report saw headline number jump to 2.4% y/y from 1.8% y/y in February but lower than 2.6% y/y as expected. The main culprit was surge in energy prices with gasoline prices jumping 21.2% m/m, the largest one-month increase ever, and 5.6% y/y. Core measures were well-behaved with median staying at 2.3% y/y, trim ticking down to 2.2% y/y from 2.3% y/y the previous month while common rose to 2.6% y/y from 2.4% y/y in February. This jump in inflation was smaller than expected and is entirely due to rising energy prices, as evident by no jumps in core reading, so BoC will not feel the need to react and we expect a pause at next week’s meeting.

This week we will have BoC meeting. There will be no change to the rate so everything will be about forward guidance.

Important news for CAD:

Wednesday:

BoC Interest Rate Decision

JPY

Kyodo went out with a report that BoJ wil likely postpone raising interest rates and will raise its inflation forecast. Trade balance surplus shrank as growth in imports overshadowed growth in exports. Import costs exploded due to the surge in energy prices while exports benefited also from rising prices.

Preliminary April PMIs showed divergence between sectors but not the one we grew accustomed to. Manufacturing PMI surged to 54.9 from 51.6 in March while a tick up to 51.8 was expected. Manufacturing output rose at the strongest pace in over twelve years as a result of strong increase in new orders. Services PMI, on the other hand, eased to 51.2 from 53.4 as domestic demand shrank. There was a slowdown in both new orders and new export orders. Inflation pressures increased in both sectors as input costs surged on the back of supply chains disruptions caused by US – Iran war. Composite PMI declined to 52.4 from 53 the previous month but still staying nicely in expansion territory and coming in above expected 51.4 print.

National inflation data for the month of March showed headline and core prints rising to 1.5% y/y and 1.8% y/y from 1.3% y/y and 1.6% y/y respectively in February but still below targeted 2%. Ex fresh food, energy component, so-called “core core”, ticked down to 2.4% y/y from 2.5% y/y the previous month. BoJ will not feel pressured by this reading to act next week but with CGPI rising hard and further increases in inflation expected in coming months we should see hikes at either June or July meetings.

This week we will have BoJ meeting. There will be no change to the rate but language of statement and Ueda’s press conference will be closely monitored for potential rate hikes in the future.

Important news for JPY:

Tuesday:

BoJ Interest Rate Decision

CHF

SNB total sight deposits for the week ending April 17 came in at CHF453.6bn vs CHF461.3bn the previous week. A bigger than usual drop but still within well-established range. Antoine Martin, the Vice Chairman of the Governing Board of SNB stated that the bank has a greater willingness to intervene given the situation in the Middle East. SNB Chairman Schlegel reiterated the message stating that they have have unrestricted room for manoeuvre with regard to the SNB policy rate and intervention in FX markets.